Do you remember the sheer amount of paperwork you signed when you bought your first home? I certainly do—my hand cramped halfway through. Now that you’re thinking about refinancing, you might be worried it’s going to be “Round Two” of that stress. But here is the good news: refinancing is often smoother, and the financial relief can be massive. Whether you want to slash your monthly payments, pay off your loan faster, or cash out some equity for renovations, getting it right the first time is crucial. In this piece, we’ll look at how to refinance a mortgage for the first time.

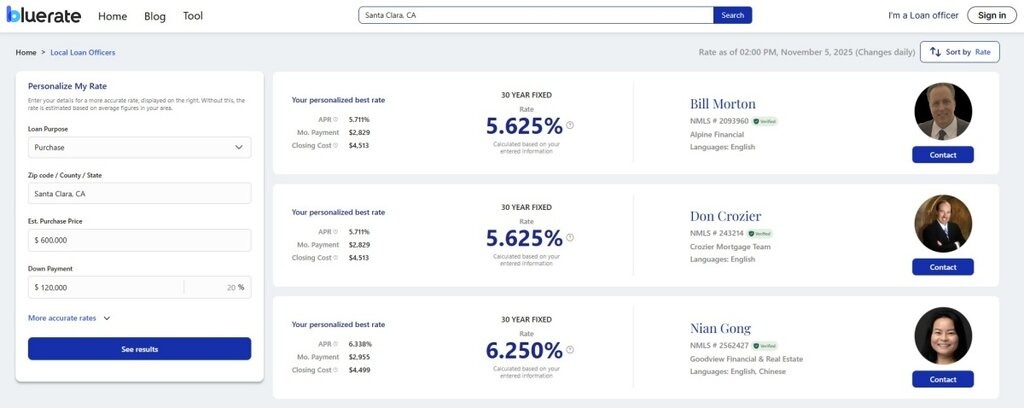

If you are feeling overwhelmed by where to start, you are not alone. My best advice? Don’t go it alone. I highly recommend hopping over to Bluerate. It’s a fantastic resource where you can consult with loan officers for free and compare rates visually. Seeing the numbers side-by-side makes the potential savings real, not just theoretical.

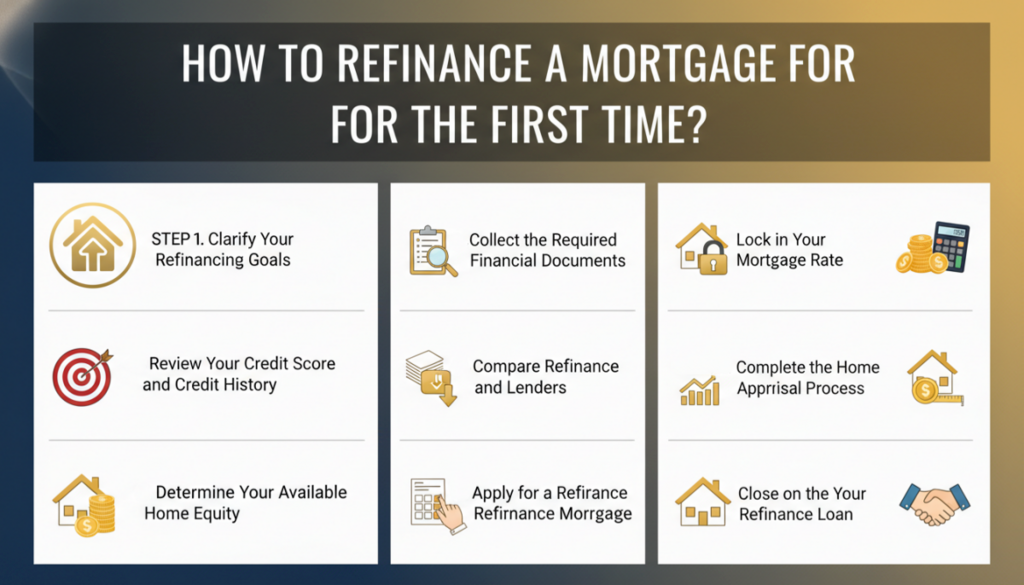

How to Refinance a Mortgage for the First Time?

Refinancing is technically just trading your old mortgage for a new one with better terms. But unlike buying a house, there is no seller and usually no moving truck involved. It is purely a financial move. However, just because it’s simpler doesn’t mean you can skip the details. A missed step here could cost you thousands in fees.

To help you navigate this, I’ve broken down the process into a clear roadmap. Think of this as your personal guide on how to refinance a mortgage loan without the headaches.

STEP 1. Clarify Your Refinancing Goals

Before we talk about interest rates, ask yourself: Why am I doing this? I’ve seen homeowners rush into a refinance just because “rates dropped,” only to realize later that they extended their loan term by five years and paid more interest in the long run. Your goal dictates your strategy.

- Lower Monthly Payments: You likely want a lower interest rate or a longer loan term.

- Pay Off Debt Faster: You might switch from a 30-year to a 15-year mortgage. Your monthly bill might go up, but you’ll save a fortune in interest.

- Cash Out Equity: If you want to renovate the kitchen or pay off credit cards, a “Cash-Out Refinance” lets you borrow more than you owe and pocket the difference.

- Stability: If you have an Adjustable-Rate Mortgage (ARM) that’s keeping you up at night, switching to a Fixed-Rate loan offers peace of mind.

STEP 2. Review Your Credit Score and Credit History

Treat your credit score like a vital sign for your financial health. When I refinanced, I checked my report a few months early and found a small error that was dragging my score down. Fixing it bumped me into a better tier, saving me about 0.25% on my rate. Over 30 years, that is huge money.

Generally, lenders look for a score of 620 or higher for a conventional loan. If you are aiming for a “Jumbo Loan” (for expensive properties), you might need a 700+. Don’t just hope for the best. Pull your free credit reports from the major bureaus (Equifax, Experian, TransUnion) and ensure everything is accurate. A higher score doesn’t just get you approved It gets you the rate that makes refinancing worth it.

STEP 3. Determine Your Available Home Equity

Step 3 in our process for how to refinance a mortgage is looking at a home’s equity. It’s simply the part of the house you actually “own.” You calculate it by taking your home’s current market value and subtracting your current mortgage balance. For example, if your home is worth $400,000 and you owe $300,000, you have $100,000 in equity.

Lenders focus on your Loan-to-Value (LTV) ratio. The magic number here is usually 20% equity. If you have less than 20% equity (or an LTV higher than 80%), you will likely have to pay Private Mortgage Insurance (PMI). In my experience, unless you are getting a drastically lower interest rate, paying PMI can eat up all your potential savings. Knowing your numbers upfront keeps your expectations realistic.

STEP 4. Collect the Required Financial Documents

Nothing slows down a refinance like a missing W-2. I learned this the hard way when my lender asked for a pay stub from a job I’d left two years prior. To breeze through underwriting, start a digital folder now.

You will typically need:

- Income Proof: W-2s from the last two years and pay stubs from the last 30 days.

- Tax Returns: The last two years of full federal tax returns (especially if you are self-employed!).

- Asset Statements: Bank and investment account statements (usually the last 2 months/quarters).

- Insurance: Proof of your current homeowners’ insurance.

Having these ready before you apply shows lenders you are a serious, low-risk borrower.

STEP 5. Compare Refinance Rates and Lenders

This is the most critical step. Many first-timers look at one bank, see a decent rate, and sign. Please don’t do that. Lenders often advertise “Teaser Rates” that require you to pay expensive “points” upfront. You need to look at the APR (Annual Percentage Rate), which includes the fees, to get the true cost.

I rely on tools that cut through the marketing noise. You may want to go to Bluerate to check your personalized rates. It allows you to see real-time data from multiple lenders tailored to your specific credit profile and equity. It’s much faster than calling five different banks, and it protects you from “bait-and-switch” offers.

STEP 6. Apply for a Refinance Mortgage

Once you pick a lender, it’s time to officially apply. You’ll fill out the Uniform Residential Loan Application (URLA). Shortly after, you will receive a Loan Estimate (LE). This is a standardized form that tells you exactly what the loan will cost, including closing costs and your estimated monthly payment.

Pro Tip: If you apply with multiple lenders within a short window (typically 14 to 45 days), the credit bureaus count it as a single “hard inquiry.” So, don’t be afraid to shop around. Compare the Loan Estimates side-by-side, specifically looking at Section A (Origination Charges) and Section B (Services You Cannot Shop For).

STEP 7. Lock in Your Mortgage Rate

Interest rates change daily—sometimes hourly. Once you are happy with the numbers on your Loan Estimate, you need to “lock” your rate. A rate lock guarantees that your interest rate won’t change between now and closing, provided you close within the specified timeframe (usually 30 to 60 days).

I once tried to “time the market,” hoping rates would drop another eighth of a percent. They went up instead. Don’t gamble. If the numbers work for your budget today, lock it in. You can ask your lender about a “float down” option, which might let you snag a lower rate if the market drops significantly before you close, though this often costs a fee.

Related: Comparison Shopping Mortgage Rates in Louisville: 5 Strategies For Success

STEP 8. Complete the Home Appraisal Process

Unless you get an appraisal waiver (which happens sometimes if you have tons of equity), the lender will order a new home appraisal. They need to verify that the home is worth enough to secure the loan.

You don’t need to do a full renovation, but treat the appraiser’s visit like a showing. Tidy up the yard, ensure safety features like smoke detectors and carbon monoxide alarms are working, and secure any pets. A lower-than-expected appraisal can derail your LTV ratio, potentially forcing you to bring cash to the table or pay mortgage insurance.

STEP 9. Close on Your Refinance Loan

Our final step on how to refinance a mortgage is the most important one. You are almost there! At least three business days before your closing date, you will receive a Closing Disclosure (CD). Compare this document line-by-line with your original Loan Estimate. They should be very similar. If there are surprise fees, ask about them immediately.

On closing day, you’ll sign the final paperwork. If you are refinancing your primary residence, federal law gives you a “Right of Rescission.” This is a 3-day cooling-off period where you can cancel the loan if you get cold feet. It’s a safety net unique to refinancing—use it if something feels wrong.

FAQs About Refinancing a Mortgage

Q1. How much to refinance a mortgage?

Closing costs typically range from 2% to 6% of your loan amount. For a $300,000 loan, that is $6,000 to $18,000. These costs include appraisal fees, title insurance, and lender origination fees.

Q2. How long does it take to refinance a mortgage?

On average, the process takes 30 to 45 days. However, in a busy market or with a complex financial situation (like self-employment income), it can stretch to 60 days. Digital lenders can sometimes close faster.

Q3. How much equity do you need to refinance?

Ideally, you want 20% equity to avoid private mortgage insurance (PMI) and get the best interest rates. However, some government-backed loans (like FHA or VA) allow refinancing with very little equity.

Q4. What is the rule of thumb for when to refinance?

A common rule is to refinance if you can lower your interest rate by 0.75% to 1%. Another method is the “break-even” calculation: divide your closing costs by your monthly savings to see how many months it takes to recoup the cost.

Q5. Are there any restrictions on refinancing?

Yes, most lenders have a “seasoning” requirement. You typically must have owned the home (or had the current mortgage) for at least 6 months before you can refinance, especially for cash-out options.

Q6. What disqualifies you from refinancing?

Common disqualifiers include a credit score below 620, a Debt-to-Income (DTI) ratio above 43-50%, having negative equity (owing more than the home is worth), or an unstable employment history.

Final Thoughts

Once you know how to refinance a mortgage and have completed the process, you’ve achieved a big financial milestone. It can free up cash flow, help you pay off your home sooner, or get rid of that pesky mortgage insurance. But as we’ve covered, the details matter. The difference between a “good” rate and a “great” rate can mean thousands of dollars staying in your pocket rather than going to the bank.

Don’t settle for the first offer that lands in your inbox. Be proactive. Take control of your financial future by comparing your options carefully. I encourage you to visit Bluerate today to find competitive lenders and transparent rates. It’s the smartest first step you can take on this journey.